|

When using TaxCalc, the tax return should automatically have the tax rate applied based on the postcode of the address on the return. Therefore the return will automatically apply the Scottish rate if there is a Scottish postcode. If this doesn't happen, please ensure that you are running the latest version of TaxCalc before trying again. If for any reason, you need to manually change the option applied by TaxCalc, please complete the below steps: SimpleStep Mode: Personal details > Your address > Select the applicable radio button on screen as to which tax rates to use.

HMRC Forms Mode: SA100 Core Return > Page 1 or click on personal details

The What if planner also provides updated calculations in line with the underlying rules applying to residents of Scotland. How do the calculations differ between the United Kingdom and Scotland?2019/2020

2018/19Below are the 2 tables based on whether the UK or Scottish tax rates are applied to the return.

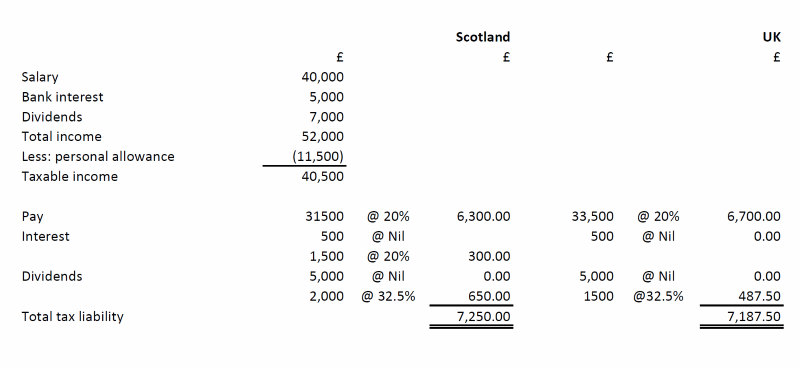

Previous years:2016/17There are no differences between the rates of tax and associated rate bands between residents of Scotland and the remainder of the United Kingdom for 2016/17. 2017/18The Scottish Government legislated to change the basic rate band to £43,000. This applies to non-savings income only, such as salary from Employment and profits from Self employment. Savings and dividend income will be assessed to tax based upon the rates of tax and rate bands applying to the rest of the UK. Below is an example of the effect of the difference in the basic rate bands have.

Please refer to the HMRC website on what the Scottish Rate of Income Tax is and how it works. |

.png)

Powered by KBPublisher (Knowledge base software)