HMRC have identified an issue whereby the Annual Allowance (pension) Charge calculated, is not always correct for Scottish rate taxpayers.

The calculation is not correct for Scottish rate taxpayers where the tax charged should be at the Scottish intermediate rate (21%-2018/19)) rather than the Scottish higher rate (41%-2018/19).

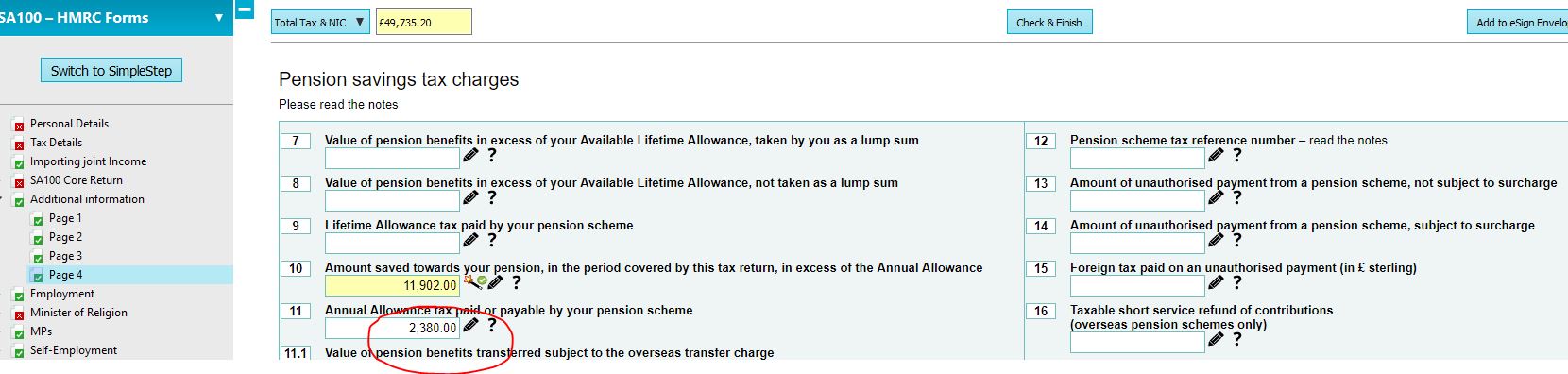

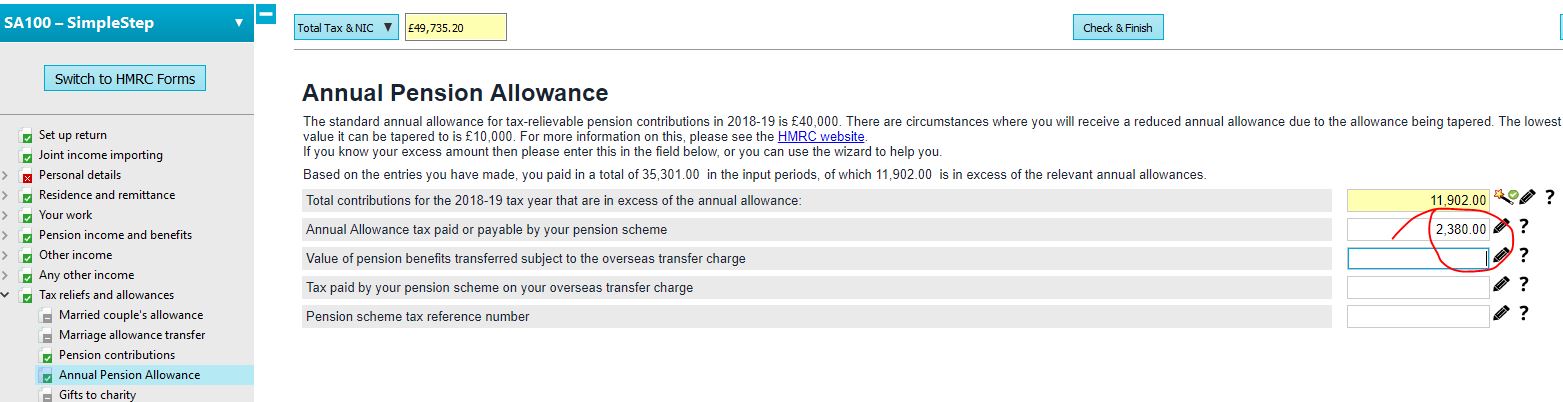

If the taxpayer is liable to pay the charge, HMRC advises a workaround to add an amount within Annual Allowance tax paid to reduce the pension charge to the expected amount.

For example, if the excess contributions are Ł11,902 and the pension charge has been incorrectly calculated @ 41% = Ł4,879, and the correct amount should be @ 21% = Ł2,499, the difference to enter in amount paid is Ł2,380.

Enter the amount as follows:

HMRC Forms mode > Page Ai4 > box 11

SimpleStep mode > Tax reliefs and allowances > Annual Pension Allowance > Annual Allowance tax paid or payable by your pension scheme.

If the pension provider is paying the charge, enter the amount paid (as above) to match the original pension charge (Ł4,897 in the above example).

If the pension provider is paying the charge, enter the amount paid (as above) to match the original pension charge (Ł4,897 in the above example).

For both workarounds, please enter details of how you arrived at the calculation stating the workaround is due to Special Case 33, in HMRC Forms mode > Page TR7 > box 19 (Any other information) or SimpleStep > Any Other income > Additional information.